The financial analysis of Nabil Bank Limited as performed by Investopaper team is as follows:

Nabil Bank Limited is the first private sector bank of Nepal. It was established in July 1984. Likewise, it is also the first joint venture bank of Nepal. Nabil Bank is the leading commercial bank of Nepal with the highest profit among private banks for several years. The bank made a profit of Rs. 3.98 billion in F.Y. 2074/75. Currently, the bank has 79 branches and 132 ATM across Nepal. Also, there are more than 1500 Nabil remit agents in Nepal. Nabil Bank has its head office at Durbarmarg, Kathmandu.

The bank also has a subsidiary company named- Nabil Investment Banking Limited. Nabil Investment Banking is a merchant banker which performs various activities such as the issue of shares, share registrars, mutual fund operation, portfolio management, etc.

Nabil Bank is currently in its 35-years of operation in the Nepalese banking sector.

Shambhu Prasad Poudyal is the current chairman of Nabil Bank. Before being the chairman, Mr. Poudyal has remained as the director of Nabil since 2004. He has excelled as the executive chairman of Rastriya Beema Sansthan from 1999-2002. The board of directors of Nabil Bank includes:

| S.N | Board Members | Post |

| 1 | Shambhu Prasad Poudyal | Chairman |

| 2 | Nirvana Kumar Chaudhary | Director |

| 3 | Pratap Kumar Pathak | Director |

| 4 | Virender Paul Dani | Director |

| 5 | Dayaram Gopal Agrawal | Director |

| 6 | Upendra Prasad Poudyal | Director |

| 7 | Malay Mukherjee | Director |

The management team of Nabil is led by Mr. Anil Keshary Shah, who currently holds the position of Chief Executive Officer (CEO) of the bank.

| S.N | Management Team | Post |

| 1 | Mr. Anil Keshary Shah | Chief Executive Officer |

| 2 | Mr. Ramesh Prasad Lohani | Chief Operating Officer |

| 3 | Ms. Namita Dixit | Chief Risk Officer |

| 4 | Mr. Gyaneshwar Acharya | Chief Corporate Officer |

| 5 | Mr. Anil Kumar Khanal | Chief- Business Officer |

| 6 | Ms. Anjuli Shrestha | Chief Finance Officer |

| 7 | Mr. Binay Kumar Regmi | Chief Marketing Officer |

| 8 | Mr. Mohan Subba | Head – Treasury |

| 9 | Mr. Yagya Prasad Sharma | Head – SME, MF, and Mid-Corporate |

| 10 | Mr. Saroj Pyakurel | Head – Consumer Lending |

Nabil is the first joint venture commercial bank of Nepal. It has 50 percent foreign ownership. General Public of Nepal holds 30 percent ownership of the bank. Likewise, Nepalese institutions possess a 10 percent share of the bank.

The ownership structure of Nabil is shown in the table below:

| Ownership Structure | Percentage (%) |

| Local Ownership | 50 |

| Institutions | 10 |

| General Public | 30 |

| Others | 10 |

| Foreign Ownership | 50 |

| Total | 100 |

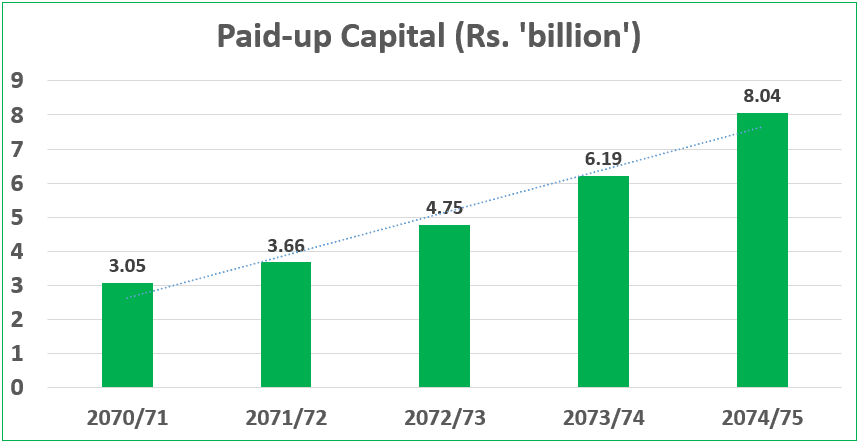

Nepal Rastra Bank (NRB), in its monetary policy 2015, directed the commercial banks to meet minimum paid-up capital of Rs. 8 billion. Due to this, Nabil bank has increased its paid-up capital to Rs. 8.04 billion by F.Y. 2074/75. The paid-up capital has grown by 26.93 percent (CAGR) in the last five years. In F.Y. 2070/71, the paid-up capital of the bank stood at Rs. 3.05 billion. In addition, Nabil has increased its capital through bonus share only. This shows the strength and profitability of the bank. The current capital (as of third quarter of F.Y. 2075/76) is Rs. 9.01 billion.

Similarly, the shareholders’ fund has grown by 25 percent compounded annually in the last five years. The shareholders’ fund was Rs. 7.64 billion in F.Y. 2070/71. It has increased to Rs. 20.59 billion at the end of F.Y. 2074/75. Also, the shareholders’ fund as of the third quarter of this fiscal year stands at Rs. 21.83 billion.

Likewise, the total assets of the bank have increased at a rate of 17 percent compounded annually. Total Assets have grown to Rs. 160.98 billion at the end of F.Y. 2074/75.

The paid-up capital, shareholders’ fund and total assets of Nabil bank in the last five years are shown in the table below:

| Fiscal Year | Paid-up Capital (Rs. ‘billion’) | Shareholders’ Fund (Rs. ‘billion’) | Total Assets (Rs. ‘billion’) |

| 2070/71 | 3.05 | 7.64 | 87.27 |

| 2071/72 | 3.66 | 9.49 | 115.99 |

| 2072/73 | 4.75 | 11.59 | 127.3 |

| 2073/74 | 6.19 | 16.7 | 144.02 |

| 2074/75 | 8.04 | 20.59 | 160.98 |

| Compounded Annual Growth Rate (CAGR %) | 26.93 | 25.21 | 17.06 |

The deposits of Nabil Bank has increased by 16.41 percent compounded annually in the last five years. At the end of the F.Y. 2074/75, the deposit collection stood at Rs. 134.98 billion. The deposit was Rs. 75.39 billion in F.Y. 2070/71. As per the unaudited third-quarter report of F.Y. 2075/76, the deposit collection of Nabil stands at Rs. 153.70 billion.

Likewise, loans and advances have grown at a steady pace at about 19 percent per annum compounded. In F.Y. 2074/75, the total loans and advances stood at Rs. 115.42. This was only Rs. 56.20 billion in F.Y. 2070/71. In the third quarter of the current fiscal year 2074/75, loans and advances of Nabil has grown to Rs. 128.20 billion.

The deposits and loans of Nabil bank in the last five years period are shown in the table below:

| Fiscal Year | Deposits (Rs. ‘billion’) | Loans and Advances (Rs. ‘billion’) |

| 2070/71 | 75.39 | 56.2 |

| 2071/72 | 104.24 | 67.16 |

| 2072/73 | 110.27 | 77.76 |

| 2073/74 | 121.84 | 94.09 |

| 2074/75 | 134.98 | 115.42 |

| Compounded Annual Growth Rate (CAGR %) | 16.41 | 19.36 |

Nabil Bank has the highest profit among the private banks of Nepal. Also, the bank has made a profit of Rs. 3.98 billion in the F.Y. 2074/75. The net profit has grown by 12.41 percent compounded annually. In the F.Y. 2070/71, the bank made a profit of Rs. 2.32 billion. Aside from F.Y. 2071/72, the bank has consistently improved its profitability. However, in the F.Y. 2071/72, the profit declined from Rs. 2.32 billion to Rs. 2.09 billion. Nabil has currently (based on the third quarter of F.Y. 2075/76) made a profit of Rs. 3.19 billion in the 9 months.

The net profit of Nabil Bank in the last five years period is shown in the table below:

| Fiscal Year | Net Profit (Rs. ‘billion’) |

| 2070/71 | 2.32 |

| 2071/72 | 2.09 |

| 2072/73 | 2.82 |

| 2073/74 | 3.7 |

| 2074/75 | 3.98 |

| Compounded Annual Growth Rate (CAGR %) | 12.41 |

Return On Equity (ROE) measures the profitability of the company on the equity provided by the shareholders. Likewise, Return On Assets (ROA) indicates the profitability of the company based on the total assets utilized. So, ROE and ROA are an important measure for the calculation of return by the company.

Nabil Bank has a high return on equity and assets. However, the ROE has declined from as high as 27.97 percent in F.Y. 2070/71 to 20.94 percent in F.Y. 2074/75. This is mainly due to the sharp rise in shareholders fund by almost 25 percent annually (compounded) in the last five years period. Whereas, the net profit has grown by only 12.41 percent during this period. Still, the ROE of 20.94 is relatively good for the banking sector.

Similarly, Return on Assets (ROA) has not declined as much compared to the ROE. ROA stands at 2.61 percent in F.Y. 2074/75. This was 2.89 percent in F.Y. 2070/71. ROA fell to as low as 2.06 percent in F.Y. 2071/72, when the profit declined.

The Return on equity (ROE) and Return On Assets (ROA) of Nabil Bank in the last five years period are shown in the table below:

| Fiscal Year | Return on Equity (ROE %) | Return on Assets (ROA %) |

| 2070/71 | 27.97 | 2.89 |

| 2071/72 | 22.73 | 2.06 |

| 2072/73 | 25.61 | 2.32 |

| 2073/74 | 22.41 | 2.69 |

| 2074/75 | 20.94 | 2.61 |

Among the commercial banks of Nepal, Nabil Bank has the highest Earnings Per Share (EPS). The annualized Earnings Per Share of Nabil Bank in current fiscal year 2075/76 is 47.69. The EPS of the bank has declined due to the huge increment in the capital. Nabil had the highest EPS of Rs. 83.68 in F.Y. 2070/71. However, EPS has declined to almost half due to the rise in the capital by more than 3 times during this period. Still, the earnings per share of Nabil is higher than its competitors.

Likewise, the Non-Performing Loans (NPL) of Nabil bank is currently at a satisfactory level. The bank is able to reduce its NPL to below 1 percent from as high as 2.23 percent in F.Y. 2070/71. The NPL has declined to 0.55 percent in F.Y. 2074/75. As of the third quarter of current fiscal year 2075/76, NPL stands at 0.64 percent. This indicates that the quality of lending of the bank has improved in the last five years period.

The Earnings Per Share (EPS) and Non-Performing Loans (NPL) of Nabil bank in the last five years are shown in the table below:

| Fiscal Year | Earnings Per Share (EPS ‘Rs.’) | Non-Performing Loans (NPL %) |

| 2070/71 | 83.68 | 2.23 |

| 2071/72 | 57.24 | 1.82 |

| 2072/73 | 59.27 | 1.14 |

| 2073/74 | 59.86 | 0.8 |

| 2074/75 | 49.51 | 0.55 |

Nabil Bank has paid good dividends to its shareholders. The bank has focused the dividend payout towards the bonus share for the purpose of capital increment. Nabil Bank reached the minimum paid-up capital requirement of Rs. 8 billion through the bonus share only. The bank has distributed bonus share ranging from 12 to 30 percent. The total dividend payout ranges from 36 percent to 65 percent. From the profit of F.Y. 2074/75, the bank has provided a dividend of 34 percent, including a 12 percent bonus share. The rate of dividend has declined in F.Y. 2074/75 due to the huge issue of bonus shares in the previous years.

The dividends provided by the Nabil Bank in the last five years is shown in the table below:

| Fiscal Year | Bonus share | Cash dividend | Total dividend |

| 2070/71 | 20 | 45 | 65 |

| 2071/72 | 30 | 6.84 | 36.84 |

| 2072/73 | 30 | 15 | 45 |

| 2073/74 | 30 | 18 | 48 |

| 2074/75 | 12 | 22 | 34 |

Nabil Bank has remained as a leading stock in Nepal share market in the commercial bank sector. It is the highest priced stock among commercial banks. During the last five years period, the market price of Nabil has fluctuated between Rs 921 to Rs 2,535 per share. The price has gradually declined from Rs. 2,535 in F.Y. 2070/71 to Rs.921 in F.Y. 2074/75. This is mainly due to the adjustment of bonus share and the market crash from 2072/73. As of today ( Ashad 2076), the market price is hovering around Rs. 800-Rs.850 per share.

Likewise, Nabil Bank has the highest market capitalization among the commercial banks of Nepal. In F.Y. 2072/73, investors valued Nabil as high as Rs. 92.88 billion. But, in the F.Y 2074/75, the market capitalization of Nabil has declined to Rs. 60.88 billion. The current market valuation of Nabil is almost Rs. 73 billion (based on Ashad 2076 price level).

The market price per share and the market capitalization of Nabil Bank in the last five years are shown in the table below:

| Fiscal Year | Market Price Per Share (MPS ‘Rs’) | Market Capitalization (Rs. ‘billion’) |

| 2070/71 | 2,535 | 59.01 |

| 2071/72 | 1,910 | 54.86 |

| 2072/73 | 2,344 | 92.88 |

| 2073/74 | 1,523 | 77.19 |

| 2074/75 | 921 | 60.88 |

In the unaudited third-quarter report of F.Y. 2075/76, Nabil Bank has shown a decent performance. The deposits and loans have increased by 14.01 percent and 17.55 percent respectively in the nine months period. The deposits stood at Rs. 153.70 billion. Likewise, the loans and advances by Nabil are Rs. 128.20 billion until the third quarter.

To View the latest performance of Nabil Bank, Click Here.

The paid-up capital of Nabil Bank stands at Rs. 9.01 billion, a rise of 12 percent. This is due to the adjustment of a 12 percent bonus share. Similarly, the bank has increased the reserves by 2.23 percent only in nine months. The reserve and surplus of Nabil are Rs. 12.82 billion until the third quarter of F.Y 2075/76.

| Headings | 3rd Qtr, F.Y. 2075/76 | Ashar end, F.Y. 2074/75 | % Change |

| Paid-up capital(Rs. ‘billion’) | 9.01 | 8.04 | 12.06 |

| Reserve and Surplus(Rs. ‘billion’) | 12.82 | 12.54 | 2.23 |

| Deposits(Rs. ‘billion’) | 153.70 | 134.81 | 14.01 |

| Loans & Advances(Rs. ‘billion’) | 128.20 | 109.06 | 17.55 |

The net profit of Nabil bank has grown by a mere 3.24 percent in a period of one year. This doesn’t look exciting. However, maintaining such a huge profit in a period of crunch in the banking credit is satisfactory. Nabil has made a profit of Rs. 3.19 billion, up from Rs. 3.09 billion in the corresponding quarter of the previous year. Despite slow growth in profit, the bank has increased its net interest income by 18 percent. Net Interest income has grown to Rs. 5.41 billion, up from Rs. 4.57 billion.

In the first nine months of this fiscal year, Nabil Bank has accumulated the distributable profit of Rs. 2.32 billion. This gives the bank the dividend-paying capacity of 34 percent (when annualized). Although the profit rose, the Earnings per share (EPS) has declined by 7.83 percent. This is due to the capital increment of 12 percent this year. Similarly, Non-performing Loans (NPL) has declined to 0.64 percent. However, the base rate has climbed slightly to 7.99 percent. Nabil Bank is one of the banks with the lowest base rate in Nepal.

The performance of Nabil Bank in the third quarter of F.Y. 2075/76 is shown in the table below:

| Headings | 3rd Qtr, F.Y. 2075/76 | 3rd Qtr, F.Y. 2074/75 | % Change |

| Net Interest Income(Rs. ‘billion’) | 5.41 | 4.57 | 18.38 |

| Net Profit(Rs. ‘billion’) | 3.19 | 3.09 | 3.24 |

| Distributable Profit(Rs. ‘billion’) | 2.32 | – | – |

| Earnings Per Share, EPS(Rs.) | 47.69 | 51.74 | -7.83 |

| Non Performing Loans, NPL(%) | 0.64 | 1.07 | -40.19 |

| Base rate(%) | 7.99 | 7.33 | 9 |

Nabil Bank has led the Nepalese banking industry since its inception 35 years ago. And, it is likely to continue to lead in the coming years. The financial performance of the bank in the last five years looks solid. The dividend payout is also relatively high. The directors of the bank are reputed business and banking personalities in Nepal. The management team of Nabil Bank is reputed and highly efficient. In conclusion, Nabil Bank is a financially strong and sound commercial bank of Nepal.

The brand of Nabil is easily recognizable. Due to its financial strength and brand loyalty, it is able to collect the funds at a lower rate. Thus, the base rate of Nabil is comparatively lower. This gives Nabil a greater competitive advantage over other banks. Nabil has huge deposits and loans portfolio. The profit is likely to increase in coming years as the liquidity situation in the economy eases. Holding Nabil stock for the long run is a viable investment strategy. Along with good dividend, an increase in the market value of the stock can be expected as the share market moves in a positive direction.

NOTE: Figures of FY 2074/75 are as per NFRS and the figures of the earlier year are as per previous GAAP. Hence, they may not be comparable.

(Investments are subject to market risks and investors are advised to do a personal homework before taking any investment decision. This material is just a guideline for the investors to do further investigations)

Read Related Contents:

Share This Via: